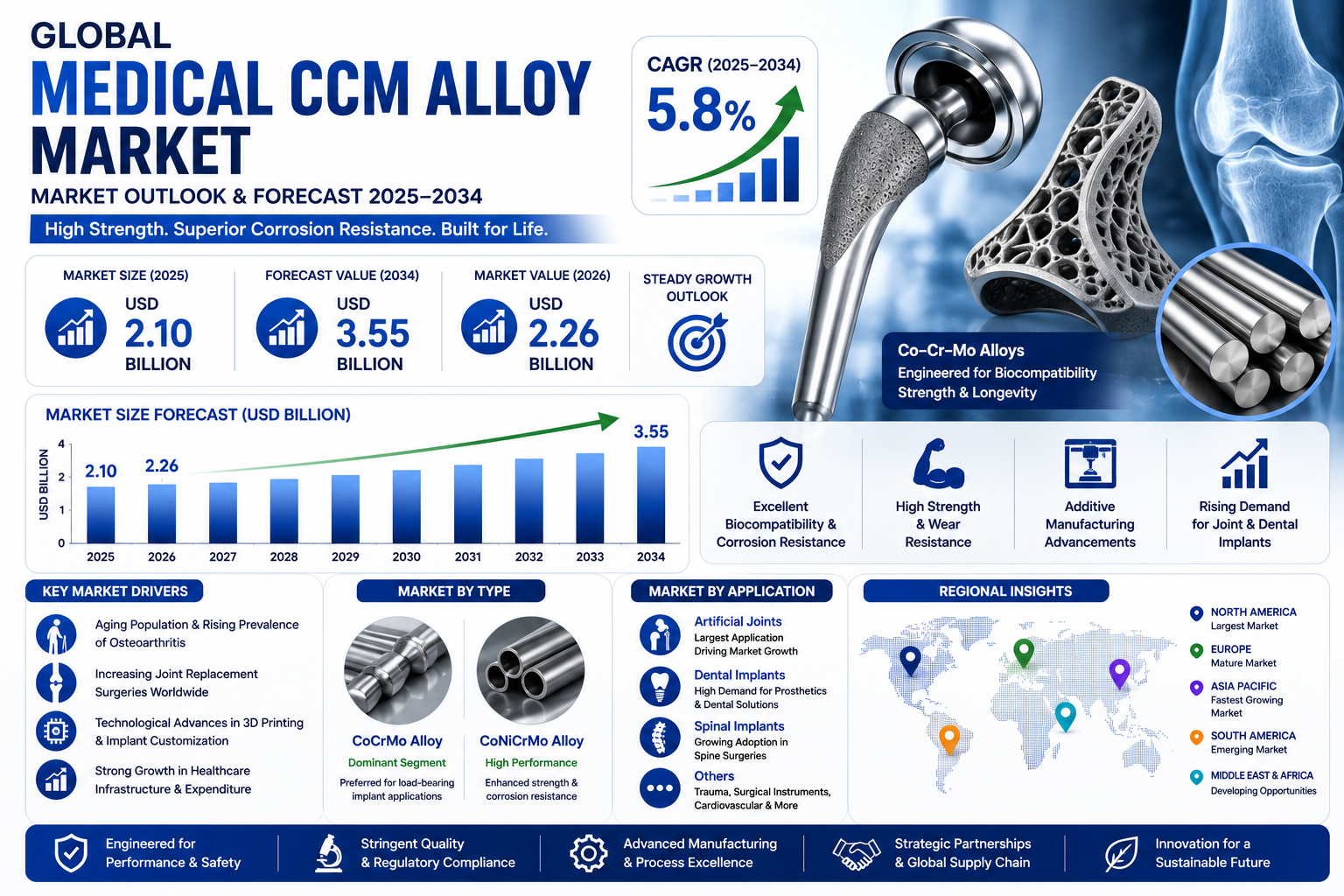

Medical CCM alloy market valued at USD 2.1 Billion in 2025, is projected to reach USD 3.55 Billion by 2034, at 5.8% CAGR.

The global Medical CCM Alloy market was valued at USD 2.1 billion in 2025. The market is projected to grow from USD 2.26 billion in 2026 to USD 3.55 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period.

Medical CCM Alloy, an abbreviation for Cobalt-Chromium-Molybdenum alloy, is a specialized metallic material engineered for medical devices and implants. Its composition is pivotal, providing an exceptional combination of biocompatibility, high strength, and superior corrosion resistance, which are non-negotiable requirements for long-term implantation in the human body. These alloys are fundamental to the structural integrity and longevity of critical orthopedic and dental applications.

The market growth is primarily driven by the rising global prevalence of osteoarthritis and osteoporosis, coupled with an aging population increasingly requiring joint replacement surgeries. Furthermore, technological advancements in additive manufacturing (3D printing) are enabling the production of highly customized, patient-specific implants, creating new demand vectors. The stringent regulatory landscape, however, presents a challenge, requiring extensive testing for biocompatibility and mechanical performance. Key players like Carpenter Technology and Fort Wayne Metals continue to innovate with high-performance grades of CCM alloys to meet evolving clinical demands.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307168/medical-ccm-alloy-market

Market Overview & Regional Analysis

North America dominates the Medical CCM Alloy market, driven by advanced healthcare infrastructure and high adoption of medical implants. The U.S. holds the largest market share due to rising orthopedic surgeries and strong presence of key manufacturers. Strict FDA regulations ensure high-quality standards for medical alloys, reinforcing the region's leadership position. Increasing prevalence of osteoarthritis and joint replacement procedures further fuels market growth. The region benefits from extensive R&D activities and technological advancements in biocompatible materials. Strategic collaborations between medical device companies and alloy suppliers strengthen the supply chain. Canada contributes significantly with its universal healthcare system supporting medical device accessibility.

The U.S. FDA's stringent approval process ensures only high-quality Medical CCM Alloys reach the market, creating trust among medical professionals and patients. This regulatory environment has positioned North America as a benchmark for product standards globally. North American manufacturers lead in developing innovative CoCrMo and CoNiCrMo alloys with enhanced biocompatibility. Continuous material improvements focus on reducing metal ion release while maintaining mechanical strength for long-term implant performance. The region houses major Medical CCM Alloy producers like Carpenter Technology and Fort Wayne Metals. These companies maintain strong distribution networks and provide customized alloy solutions for various medical applications. Rising geriatric population requiring joint replacements drives steady demand. Growing awareness about advanced orthopedic treatments and increasing healthcare expenditure support market expansion across the region.

Europe represents a mature Medical CCM Alloy market with Germany and France as key contributors. The region benefits from well-established healthcare systems and high penetration of medical implants. Stringent EU medical device regulations ensure product safety and performance standards. Growing preference for minimally invasive surgeries enhances alloy demand for smaller, durable components. The presence of specialty alloy manufacturers like Aubert & Duval supports local supply chains. Countries with aging populations show consistent demand for joint and spinal implants. However, price pressures from generic implants pose challenges to premium alloy adoption in some markets.

Asia emerges as the fastest growing region for Medical CCM Alloys, led by China and Japan. Expanding medical infrastructure and rising disposable incomes boost access to advanced treatments. China's domestic manufacturing capabilities have significantly improved, reducing import reliance. Japan leads in precision medical devices requiring high-performance alloys. Southeast Asian countries witness increasing medical tourism for orthopedic procedures. However, price sensitivity remains a constraint in developing markets. Local manufacturers focus on cost-effective solutions while maintaining essential quality parameters. Regulatory harmonization efforts aim to improve product standards across the region.

The South American market shows moderate growth potential, with Brazil as the largest consumer. Economic fluctuations impact healthcare investments and medical device adoption rates. Brazil's well-developed orthopedic sector drives steady demand for quality alloys. Argentina faces challenges due to import restrictions and limited local production capabilities. Increasing awareness about advanced medical treatments creates opportunities for market expansion. Regional manufacturers focus on developing affordable alloy solutions for local needs. Infrastructure limitations in remote areas affect market penetration in some countries.

The MEA region presents niche opportunities in the Medical CCM Alloy market. Gulf countries like UAE and Saudi Arabia lead in adoption due to high healthcare spending and medical tourism. Israel shows advanced capabilities in medical technology development. Africa faces significant challenges including limited healthcare infrastructure and affordability issues. Some countries rely on donated medical equipment rather than new implants. However, market potential exists in urban centers with improving healthcare services. Regional partnerships aim to enhance local manufacturing capabilities over time.

Key Market Drivers and Opportunities

The global medical CCM alloy market is experiencing robust growth due to rising demand for orthopedic and cardiovascular implants. CCM (cobalt-chromium-molybdenum) alloys offer superior biocompatibility and mechanical properties, making them ideal for joint replacements and stents. The aging population requiring these procedures has grown by approximately 18% over the past decade.

3D printing technologies are revolutionizing customized medical implants, with CCM alloys being a preferred material due to their excellent printability and post-processing characteristics. The medical 3D printing sector has shown a compound annual growth rate of 23% since 2018, directly fueling CCM alloy demand.

North America accounts for 42% of global medical CCM alloy consumption, driven by sophisticated healthcare infrastructure and high procedure volumes. Regulatory approvals for new CCM alloy formulations continue to expand clinical applications, with over 15 new FDA-cleared devices incorporating these materials since 2020.

The dental industry presents significant growth potential for CCM alloys, particularly in high-end prosthetics and implant-supported bridges. Market projections indicate a 19% increase in CCM adoption for dental applications by 2026, driven by their superior wear resistance in occlusal applications.

Recent innovations in nickel-free CCM formulations address allergy concerns while maintaining mechanical properties. These advanced alloys are capturing a growing segment of the market, with adoption rates increasing by 35% among patients with metal sensitivities.

Challenges & Restraints

While CCM alloys offer exceptional performance, their production involves expensive raw materials requiring precise metallurgical control. Manufacturers face a 25-30% higher production cost compared to conventional implant materials, impacting market accessibility in price-sensitive regions.

Medical CCM alloys require exhaustive biocompatibility testing and documentation, often delaying time-to-market by 12-18 months compared to industrial applications. Titanium alloys and PEEK polymers continue to capture market share in certain applications due to lower costs and comparable performance in non-load bearing implants.

The specialized composition of medical CCM alloys makes post-consumer recycling economically challenging. Less than 15% of medical CCM waste currently re-enters the production cycle, creating sustainability concerns that may impact long-term adoption rates in environmentally conscious markets.

Market Segmentation by Type

● CoCrMo Alloy

● CoNiCrMo Alloy

CoCrMo Alloy remains the preferred choice due to its superior biocompatibility and mechanical properties required for load-bearing applications in medical implants. The cobalt-chromium composition provides excellent wear resistance and durability critical for orthopedic devices.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307168/medical-ccm-alloy-market

Market Segmentation by Application

● Artificial Joints

● Dental Implants

● Spinal Implants

● Others

Artificial Joints dominate application segments as CCM alloys demonstrate exceptional performance in total hip and knee replacements. Their high strength-to-weight ratio and resistance to body fluids make them ideal for joint reconstruction applications with long-term implantation requirements.

Market Segmentation and Key Players

● Carpenter Technology (United States)

● Aubert & Duval (France)

● Fort Wayne Metals (United States)

● Banner Medical (Germany)

● ATI Metals (United States)

● DSM Biomedical (Netherlands)

● AMETEK Specialty Metal Products (United States)

● Zapp Precision Metals (Germany)

● ThyssenKrupp Materials NA (Germany)

● Daido Steel (Japan)

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Medical CCM Alloy, covering the period from 2025 to 2034. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

● Sales, sales volume, and revenue forecasts

● Detailed segmentation by type and application

The report features in-depth competitive intelligence including:

● Market share analysis of leading manufacturers

● Production capacity expansions

● Product portfolio assessments

● Strategic partnership evaluations

Our research methodology combines primary interviews with industry leaders and comprehensive data analysis of:

● Production facilities and their geographical distribution

● Raw material sourcing patterns

● End-user industry consumption trends

● Regulatory impact assessments

Get Full Report Here: https://www.24chemicalresearch.com/reports/307168/medical-ccm-alloy-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

● Plant-level capacity tracking

● Real-time price monitoring

● Techno-economic feasibility studies

With a dedicated team of researchers possessing over a decade of experience, we focus on delivering actionable, timely, and high-quality reports to help clients achieve their strategic goals. Our mission is to be the most trusted resource for market insights in the chemical and materials industries.

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/

Follow us on LinkedIn: https://www.linkedin.com/company/24chemicalresearch